INITIAL COIN OFFERINGS

Issues Paper

CONSULTATION PROCESS

Request for feedback and comments

This Issues Paper forms part of Treasury’s review into Initial Coin Offerings (ICOs). The Treasury invites interested parties to make submissions on any or all aspects of the issues raised in this paper by 28 February 2019. Submissions may be lodged electronically or by post. Feedback gathered during this process will inform subsequent advice to the Government.

Closing date for submissions: 28 February 2019

Email: [email protected]

Mail: Division Head

Financial System Division

The Treasury

Langton Crescent

PARKES ACT 2600

Inquiries: Enquiries can be initially directed to [email protected]

Phone: 02 6263 2111

Responses will ordinarily be published on the Treasury website as submissions to the inquiry. You need to expressly state if you do not want us to publish your name.

INITIAL COIN OFFERINGS

What You Will Learn

Introduction

The Australian Government has identified innovations in financial technology – or “FinTech” – as potentially transformative for the Australian economy. Australia’s ambition is to be a global leader in technology and financial innovation that will contribute to productivity and economic growth, as well as the efficiency and inclusiveness of the financial system over the long term.

A relatively recent financial innovation that is attracting much attention, both domestically and globally, is the so-called initial coin offering (hereafter, ICO). ICOs, which rely on distributed ledger technology (DLT), emerged as a niche form of private fundraising within the technologically sophisticated developer community. ICOs have since taken on public appeal, with offers being made to mass retail investors. Although ICOs have some parallels with Initial Public Offerings (IPOs), venture capital and crowdfunding, the ways in which they are structured can be quite distinct from existing forms of capital raising.

These distinctions, and rapid growth in the popularity of ICOs, are testing regulatory frameworks around the world. The technology underpinning an ICO means that geographic borders are relatively easily traversed and there is widespread anecdotal evidence to suggest that the organizers of ICOs are choosing to issue from jurisdictions where regulatory settings are seen as most accommodating. A number of jurisdictions are actively competing to attract ICO activity and establish themselves as a hub for innovative technology companies that favor ICO fundraising.

At the same time, regulators in many jurisdictions have expressed significant concerns over the potential risks posed by ICOs to consumers and investors. Reports of fraud and investor loss are numerous and there is also anecdotal evidence that many ICOs have been conducted based on an often incorrect assumption that existing financial regulations do not apply.

This paper is intended to solicit the views of interested parties on the opportunities and risks posed by ICOs for Australia; whether our regulatory framework is well placed to allow those opportunities

to be harnessed whilst appropriately managing the associated risks; and, whether there are other actions that could be taken to best position Australia to capitalize on new opportunities.

Definitions and token categories

While there is no widely-adopted definition of an ICO, it typically involves the creation of digital tokens by an issuer using distributed ledger technology (DLT). The tokens are acquired by investors and potential consumers through online auction or subscription, typically in exchange for a cryptocurrency such as Bitcoin or for official fiat currency such as United States dollars.

In essence, tokens are a medium of exchange within a DLT-based business venture, allowing token holders the ability to earn value and/or to spend their tokens on services that are internal to the venture. While ICOs are often compared with crowdfunding, these two public online fundraising methods differ in some important respects (refer to Box 1).

Challenges in categorizing ICO tokens

Digital tokens issued in an ICO, or crypto-tokens, generally have certain rights attached2 which grant to holders:

• The right to another digital currency (a ‘currency’ token, commonly referred to as a ‘stablecoin’);

• The right to a promised future cash flow linked to an underlying business or investment (an ‘equity’, ‘asset’ or ‘investment’ token); or

• the right to access a product or service provided by the issuer usually at some future point in time (a ‘utility’ or ‘access’, token).3

Neatly defining and categorizing digital tokens into one of the above types can be difficult for a number of reasons. Some tokens, for instance, confer on their holders a combination of rights such as access to products and services, profit sharing and the ability to vote. Other tokens may evolve into another type of token as the project develops – such as by starting as a token that represents a financial interest in the project and later used to purchase a good or service available through the network on which it was created. In addition, the rapid pace at which the industry is developing means that new types of tokens are constantly being issued – and these tokens may not fit neatly into the categories identified above.

If a token has the characteristics of a financial product – for example, it confers rights to an equity stake in a business – it is often referred to as ‘security’ token in general discussion. It is important to note that a token may be a financial product even if it is described by another name, such as a utility token. As a result of the varied and dynamic nature of ICO tokens, and the fact that ICOs represent a new form of fundraising, it is difficult to make general and definitive statements on the application of existing regulatory frameworks to all ICOs. For example, while some digital tokens such as ‘equity’ tokens bear the hallmarks of a financial product, others such as utility tokens are more difficult to assess. This is discussed in more detail below (refer to ‘Regulation of ICOs – Global regulatory approaches and challenges’).

benefited from the network effects inherent to the ICO fundraising model, and heightened interest

surrounding digital tokens in recent years, which has fuelled speculation and market growth.

Investor exuberance and speculation

There is a range of reasons why ICOs are perceived by some investors as an attractive alternative to

more traditional methods of investing. In particular, members of the public who are not sufficiently

large-scale to be an angel or venture capital investors consider ICOs to be a valuable opportunity to

purchase digital tokens in start-ups at an early stage, rather than wait for shares to be offered

through IPOs. While speculative investor behavior has emerged as a key driver of the proliferation

of digital tokens, well-publicized losses and outright frauds have recently tempered some of this

optimism.

Digital token exchanges

The growth of digital token exchanges (and digital wallet providers) has facilitated digital token

trading. This has supported the growth of ICOs by providing liquidity for more popular tokens. Where digital tokens are traded on an exchange, this makes it easier for investors to find tokens that they are interested in buying. In addition to providing a marketplace for trading digital tokens, digital token exchanges may also create an opportunity for investors to crystallize any rise in the value of their tokens or to exit a loss-making position.5

For ICOs that are not equity sales, the business is able to retain full equity ownership and control which is a significant motivating factor for some start-ups. In some cases, tokens issued may have no rights attached to them, and so the money received is effectively a donation. By remaining a private company, firms may also avoid incurring the costs typically associated with public reporting requirements.

ICO tokens may be issued to a large number of small investors. Tapping into new investor groups creates an additional funding source for businesses, and may be an attractive option for start-ups that are not yet mature enough to access venture capital or to undertake an IPO.7For some Australian businesses, accessing new sources of capital has also allowed them to stay onshore rather

than relocating overseas in search of capital.

Creating a unique token allows the business to retain more control of its blockchain and its ecosystem, including by determining total supply. In addition, raising funds through a digital token offering may make the business’s product or service more attractive to consumers who are interested in crypto-related products and services. This can also create value through network effects, by turning customers into advocates and fostering a community that is attached to the business brand from the time of launch.

Finally, the functionality of digital tokens can allow for transactions on the businesses’ platform to take place without requiring the services of traditional payment and settlement intermediaries typically required for transactions involving fiat currencies. In contrast with the way in which businesses typically transact across borders, a digital token enables a singular payments system that obviates the need to operate in multiple fiat currencies.

For consumers and investors

An ICO may allow individual investors to gain exposure to a startup or small business in the early stages of growth, and/or provide access to a product or service that they value. Depending on what is promised, the digital token received may allow consumers to earn bonuses and discounts on a product or service or function as a loyalty rewards program. In addition, compared with traditional venture capital where investors’ equity may be tied up for many years, equity in the form of a digital token may provide investors with more immediate liquidity where a secondary market exists for the tokens owned.

While industry and media reports indicate that a large number of digital tokens lose value after the ICO, token-holders may benefit if the token’s value appreciates over time. Further, the digital tokens offered via ICOs may, over time, become a more accepted asset class in a diversified investment portfolio.

In theory, an enterprise using DLT, such as through an ICO, has the potential to reduce counterparty risk for consumers and investors by hard-coding rights into a ‘smart contract’ on the blockchain (if any rights exist). This may result in a technologically secure way of providing consumer and investor protections. A smart contract is essentially an algorithm that executes an automatic transfer of digital assets, money, or utility between parties when pre-defined events occur, removing the need for an intermediary to ensure the parties’ rights under the contract are fairly executed.

For the economy

A number of jurisdictions are actively competing to attract ICO activity and establish themselves as a hub for innovative technologies that favor ICO fundraising. Industry proponents see ICOs as having the potential to help fuel innovation-driven economic growth, although it is too early to tell what might be the long-run benefits.

It has been suggested that ICOs have become a significant source of funding for some start-up

projects. Future growth in ICO popularity could potentially create competition with traditional forms of fundraising, generating greater efficiencies across the financial system. So long as the incentives faced by fundraisers and investors are sufficiently aligned, ICOs could help to improve the efficiency of capital allocation and contribute to economic growth.

Further, an ICO-friendly jurisdiction may attract ancillary services and this, in turn, may generate positive flow-on effects for the wider economy. Examples of such services include digital token exchanges and wallet providers as well as legal and financial consulting services. In particular, it is reasonable to expect that increased ICO activity would result in law and professional services firms investing in these capabilities as well as new specialist firms entering the market.

Risks

For industry

A large number of ICOs have failed, and many have turned out to be scams or have raised money illegally from public investors due to non-compliance with regulatory obligations. The resulting ‘wild

west’ notoriety of the ICO industry has challenged the reputation of some legitimate businesses, and

even technologies, related to ICOs. Another key concern raised by businesses considering raising funds via an ICO is the legal and regulatory risk due to uncertainty or unfamiliarity on the application of the regulatory regime.

There is also a high degree of uncertainty as to how much money will be raised by an ICO. Given the

increasing effort and cost involved in preparing for an ICO funding round, businesses may also underestimate the upfront costs involved. There may also be challenges in valuing the business and estimating the future financial needs of the business, given the volatility of token prices and that digital tokens may be listed at different prices on various exchanges.

For consumers and investors

Early generation ICOs attracted participation from investors who were technologically sophisticated

and were likely to be familiar with the parties seeking to raise funds, and the underlying technology being used. As ICOs have become more popular, many newer investors do not or cannot undertake the due diligence required to have a full understanding of the risks involved with either the technology being used or the investment itself. As a result, risks to consumers are now being highlighted by regulators through published statements.8

Financial risks to consumers can be particularly high; while data on ICO activity is incomplete, recent reports indicate that a significant proportion of ICOs fail or are fraudulent, with the number of successful ICOs are as low as 7 per cent in 2017 and the majority of financial gains accruing to private parties who invested prior to the public ICO taking place.9 Depending on how an ICO is structured, the digital tokens offered under an ICO may fall outside the scope of existing financial regulation, in which case investors are not protected. Further, given the cross-border nature of ICOs, legal protection and avenues for recourse may be limited, including if the tokens are lost or stolen

(for example, via hacking or the loss of private access keys).

Extreme volatility in the value of new digital tokens also exposes consumers to significant risk. While much of this volatility reflects inherent uncertainty over the true value of the tokens, it may also be driven by instances of market manipulation. In a large proportion of cases, tokens will have been offered to private investors in a ‘presale’, sometimes with significant discounts of up to 80 per cent. Those initial investors may seek to create an undue level of hype surrounding the offering in order to sell their tokens at an artificially inflated initial trading price, before the value of the tokens decline markedly (so-called “pump and dump” schemes).

In addition to the traditional financial risks of investing in early-stage startups, retail investors in ICOs may find that the rights attached to digital tokens do not accord with their expectations or do not exist. ‘White papers’ are the typical disclosure document where ICO issuers detail mission statements, employee biographies and the technical specifics of a project – however, these documents often lack detailed, consistent information and some contain fraudulent claims or plagiarised language. Misrepresentations made by token issuers over the specific rights attached to the tokens, or the prospect of significant potential or guaranteed returns, is an area that has the potential to be of significant harm to consumers.

There are also operational risks if the platform, product or service fails or does not perform as expected, leaving the consumer with worthless digital tokens. Further, risks surrounding digital infrastructure security have materialized internationally, particularly in relation to digital wallet providers and cryptocurrency exchanges.10

For the economy

While the advent of a new mechanism which could direct capital efficiently to innovative companies

has the potential to deliver real economic gains, the realisation of those gains partly depends on the incentives faced by investors and those seeking to raise the capital. The exuberance surrounding ICOs has been evidenced by a rapid increase in the number of ICOs brought to market in a relatively short period of time, and in the volume of funds raised, with individual ICOs raising funds well in excess of expectations and often on the basis of scant, or at times fraudulent, information about the underlying company, its prospects and the rights of investors.11

The historical record demonstrates that such signs of overexcitement can be associated with instances of speculative excess, fraud and capital misallocation. This can ultimately lead to lower returns on investment with deleterious impacts on overall economic growth. A large number of failed ICOs and instances of significant consumer and investor loss could also tarnish views on DLT more generally and reduce people’s willingness to learn about and invest in its genuine economic potential. Further, a large-scale ICO failure may undermine investor trust and confidence in our regulatory system and harm Australia’s reputation for having a well-regulated financial sector.

Emerging fund-sourcing mechanisms such as crowdfunding could also be undermined in the event of large-scale ICO failure, potentially resulting in negative investor sentiment towards non-traditional forms of fundraising. Such an outcome would be expected to limit new and existing businesses’ ability to capitalize on a full range of fundraising capabilities, hindering business growth.

Although the ICO market is small relative to the broader economy, new digital tokens are being created at a rapid pace and, if current trends were to continue and tokens became widely adopted in mainstream society, this could ultimately create difficulties for macroeconomic management. Digital

tokens, at least to date, have been subject to wide swings in value. Should individual and institutional investor exposure to digital tokens continue to grow, the financial stability implications of this volatility could become non-trivial. Further, much wider adoption of digital tokens as a means of payment could eventually present some challenges for monetary policy.

Regulation of ICOs

Internationally, some countries are actively seeking to attract and develop a vibrant ICO market, while others have banned crypto-token activity entirely. Within Australia, ICOs are subject to Australian Consumer Law where the tokens issued are not classed as financial products.12 If the tokens issued are classed as financial products, the ICO is subject to the Australian Securities and Investments Commission Act 2001 (ASIC Act).

Global regulatory approaches and challenges

In general, financial market regulators are taking various steps to clarify how existing laws apply to cryptocurrency trading or issuance, while in the case of some smaller markets, new bespoke frameworks have been created, often through targeted legislation. Aside from specific regulatory approaches, the relative attractiveness of jurisdiction as an ICO host may be influenced by tax settings, the vibrancy of its local FinTech and startup ecosystem, and various other characteristics or conventions of that country or state.

Some jurisdictions (such as China13 and South Korea)14 have banned or actively sought to suppress

cryptocurrency trading or issuance (including ICOs). According to public statements, regulators in such jurisdictions are largely driven by concerns of fraudulent activity and scams. In the most extreme cases, the use, creation, and sale of cryptocurrencies may be prohibited by law and punishable by imprisonment.

Actions that may be taken to enforce a ban include banning banks from dealing with businesses involved in exchanging or processing digital assets, blocking access to websites, the forced closure of exchanges, and placing restrictions on search engines and social media platforms. However, there are significant practical challenges in enforcing a complete ban, given the decentralized and global nature of digital tokens.

Other regulatory responses have been to issue statements to warn consumers and investors of the risks associated with ICOs and to put ICO organizers on notice that their activity is being monitored.15 The United States’ Securities and Exchange Commission (SEC) and Europe’s European Securities and Markets Authority (ESMA)16 have taken steps to clarify how existing regulations apply to ICOs. In addition, some jurisdictions have announced they are analyzing ICO developments and may move to regulate the sector more actively in the future.17

Identifying when an ICO falls within financial services or securities laws

One of the key challenges for market participants and regulators in accommodating ICOs within existing frameworks has been determining when an ICO token is a “financial product” and thus falls within relevant financial services and securities laws. Uncertainty of whether and how to comply with financial services regulations appears to have constrained some jurisdictions’ digital token issuance.

If an ICO token is subject to financial services or securities laws, issuers are expected to comply with

specific obligations as they might apply to those undertaking an IPO, the sale of an options contract, or the sale of units in a managed fund. This could require token issuers to prepare detailed disclosure documents, complete independent audits, hold certain licenses, submit specific reports to regulators and comply with a range of financial market provisions.

There are some challenges in applying financial services and securities laws to ICOs

Where a digital token grants the holder an equity interest, a right to expected future cash flow, or

where its value is linked to the performance of a real or financial asset, it may be self-evident that it is a financial product. However, in many cases, this determination is less straightforward. This can be for a number of reasons, for example where the digital token performs multiple functions at different times during the project life-cycle, or where there is a lack of detail surrounding a clearly defined business plan about the digital token and its attached rights and obligations, the project or company to which it is attached, or the broader features of the enterprise.

To address the challenges in characterizing certain digital tokens as a type of financial product, some

regulators have considered factors such as: how the token is marketed, including whether the product is described as an investment opportunity; and whether the token is exchangeable for an existing good or service, or if the platform is yet to be developed.

The United States Securities and Exchange Commission (SEC), for example, has deemed that tokens

are securities if they represent an investment in a common enterprise with an expectation that profit will be derived from the efforts of others – the so-called ‘Howey test’. Statements issued by the SEC have been interpreted by industry as an indication that ICO tokens will generally be treated as securities (refer to Box 2).

Some jurisdictions have made formal determinations of sub-categories of

digital tokens

Some international regulators may identify certain digital tokens as being subject to financial services and securities laws, and other digital tokens that are subject to separate rules. For example, Switzerland’s financial market regulator defines three categories of tokens, including ‘payment tokens’ which provide access to a platform, and are therefore subject to anti-money laundering (AML) laws but not to securities laws (refer to Box 3).

Policymakers in Malta have enacted a new set of laws that define various categories of tokens, including ‘virtual financial assets’ which are subject to separate rules from financial products.19

Similarly, the Wyoming state government20 in the United States has implemented measures to exempt utility tokens from certain financial services laws, so long as the tokens are exchangeable for goods and services, and not marketed as investments.21

However, costs and benefits must be weighed

Anecdotal evidence suggests that while formal determinations of what regulatory obligations apply to digital tokens have reduced uncertainty for some businesses, it has created a significant regulatory burden. For example, some industry participants have reported that a determination from Switzerland’s financial regulator can take up to six months.

Rather than distinguishing between financial product tokens and other types of digital tokens, some

jurisdictions apply frameworks that allow all ICO fundraising to take place outside of financial services or securities laws. This means that tokens are sold without the disclosure and reporting requirements that traditionally accompany a financial product, regardless of the token’s structure.

For example, the Isle of Man’s financial regulator has determined that tokens are not investments for regulatory purposes and that virtual currency businesses are not subject to supervision or regulation by the regulator, other than compliance with AML laws.22 While this is a straightforward approach that provides certainty for digital token issuers, it may skew incentives towards ICO fundraising over other forms in order to avoid regulation. On the other hand, it could discourage some participants that may consider unregulated ICOs highly risky compared to regulated forms of investment.

It should be noted that regulations in the consumers’ jurisdiction may apply even if the ICO is hosted in a different jurisdiction.

Regulatory frameworks in Australia

The emergence of ICOs as a new mechanism for capital raising has increased interest in the applicability of Australian financial services law to ICOs, and industry participants are seeking clarity on when and how to apply financial product law.

Protection of consumers and investors

The Australian Consumer Law is the principal consumer protection law in Australia. It sets out prohibitions that apply generally to all businesses that operate in Australia. These prohibitions cover

unfair contracts, unfair practices, unconscionable conduct, and misleading or deceptive conduct. With respect to financial products and services, similar protections are afforded by the Australian Securities and Investments Commission Act 2001 (ASIC Act). Consumer protection law for financial products and services is supervised by ASIC, while consumer protection law for non-financial products is generally supervised by the Australian Competition and Consumer Commission (ACCC).

The overarching policy intent of these provisions is to protect consumers and investors from misleading and deceptive conduct, representations and practices across a broad range of consumer and financial products and services. The prohibition against misleading and deceptive conduct is also intended to influence norms for business conduct in the marketplace.

In the case of ICOs subject to consumer law (that is, not financial products), the ACCC has delegated

its powers to take action against misleading and deceptive conduct to the Australian Securities and Investments Commission (ASIC). Consumer protection provisions apply to ICOs whether or not they are financial products, consistent with the broad policy intent of the provisions. Feedback from

industry groups in Australia suggests that the application of consumer law to ICOs is currently appropriate.

Regulation of financial products

Additional provisions apply to financial products and services as outlined in the Corporations Act 2001 (Corporations Act) which is administered by ASIC. These laws set out the compliance and reporting obligations that companies have when they form, operate and cease and the obligations applying to the provision of financial products and services.

A financial product under the Corporations Act includes a managed investment scheme (MIS), share

offering, derivative, or a non-cash payment facility (refer to Box 4, below). The Corporations Act can require those that deal in such financial products to be licensed (subject to some exemptions) and to comply with disclosure, registration and other obligations in relation to offering a financial product. Box 4 also provides some general information on the obligations which may apply to issuers of financial products. More detailed information on when an ICO token might be a financial product and the obligations which may apply can be found in ASIC guidance: Information Sheet 225.23

Industry-led initiatives

In addition to formal regulation, the industry has a collective role in establishing minimum standards and raising governance levels in order to foster consumer and investor confidence. One prominent international example is the Simple Agreement for Future Tokens (SAFT) project, which was formed with the aim of developing an industry standard for digital token sales that are compliant with regulatory frameworks in the US and elsewhere. Similarly, a Code of Conduct has been developed by an industry body for digital finance, Global Digital Finance, setting out principles for token issuance and other crypto asset activities.

While industry-led initiatives can play a role, many in the industry believe that an appropriate level of regulation is welcome and that self-regulation alone is not an optimal path forward. It has been noted that where government and regulators are clear on how legal frameworks apply to ICOs, and are willing to accommodate innovation, this provides certainty and contributes positively to the development of the industry, particularly given the ‘wild west’ notoriety the sector has gained in its infancy.

New regulatory frameworks

Some industry participants have suggested that a new regulatory framework, separate from current financial services law, would best support the development of an ICO market in Australia. A recent comparable example is the Corporations Amendment (Crowd-sourced Funding) Act 2017, which established a new legislative framework for fundraising via crowdsource platforms. Such bespoke frameworks have the potential to provide clarity of the application of relevant laws and regulations and encourage economic activity.

However, the costs of introducing a new regulatory regime must be weighed against any potential benefits, particularly if the existing regime may be generally sufficient or where other measures could be taken to achieve policy goals. Disadvantages could include adding unnecessary legislative complexity and stifling future innovation by locking in particular ICO models. In addition, there can be a significant lead time involved in setting up a new legislative framework, and this should be taken into account given the rapid pace of change in ICO and DLT-based businesses.

Some adjustments to the current regime could be considered in order to provide more regulatory certainty and remove any impediments to legitimate ICO fundraising. For example, an area where more certainty might be beneficial is the distinction between security and utility tokens, and the associated application of consumer and financial services laws. Such clarity could potentially be provided through further regulatory guidance, or via legislative change.

Tax treatment of ICOs

The current tax treatment of ICOs follows from the attributes of the tokens that are issued. This tax treatment is consistent with the taxation of other commercial transactions, financial instruments and capital raising mechanisms, where the tax implications flow from the underlying nature of the rights and obligations attached to the instrument, and not the form in which the instrument is issued.

For example, some ICOs offer tokens with equity-like characteristics in the form of voting rights or profit participation, while other ICOs offer tokens that give rights to the future use of a DLT platform. As a result, how proceeds from ICOs are taxed in the hands of the issuer will depend on a number of factors, including whether they are issued in the form of a managed investment scheme, an offer of shares or other forms of equity, an offer of a derivative, or non-cash payment facility (potentially for future services to be provided by the issuer), in the same way as any other transaction or event.

Tax law contains tests to determine whether a particular interest is a debt interest or an equity interest (or neither) for tax purposes. These ‘debt and equity tests’ may impact the tax treatment of the proceeds of the ICO (both in the hands of the issuer and the investor), including whether a return on an interest in an entity may be frankable and non-deductible to the issuer (like a dividend), or whether it may be deductible to the issuer and not frankable (like interest).

Tax implications for issuers

Given the variety in how these arrangements can be structured, there is no single manner in which

ICO proceeds are taxed. The following non-exhaustive list of scenarios outlines a range of possible

tax outcomes:

• Where the tokens are issued in respect of a debt or equity instrument, the issue proceeds may not be assessable up front to the issuer.

• Where the tokens are issued in respect of prepayment for a service, the issue proceeds are likely to be assessable to the issuer.

• If the issuer of the tokens makes regular transactions in tokens, it is possible that the proceeds could be seen as forming part of some trading activity such that the ICO proceeds could be taxed as ordinary income.

• Proceeds from tokens that are issued as an offer of a derivative could be subject to tax under the taxation of financial arrangement rules.

Tax implications for token holders

For the token buyer or recipient, tokens acquired through an ICO are considered an asset for tax purposes, and any capital gains arising may be subject to capital gains tax (GST). Alternatively, gains

can be taxed as ordinary income, depending on the purpose of the acquisition.

Tokens that are acquired and used solely for the purchase of goods and services for personal use or consumption may be considered a personal use asset. Capital gains on personal use assets acquired for less than $10,000 are disregarded for tax purposes. All capital losses made on personal use assets are disregarded.

Like other assets within the CGT regime, a token is considered to be disposed when it is sold, traded

or exchanged. For example, this can include converting cryptocurrency to a fiat currency such as Australian dollars, using it to obtain goods and services or exchanging one cryptocurrency for another cryptocurrency.

There may also be tax consequences that arise in relation to returns or flows of value that may be received by taxpayers who hold tokens acquired through an ICO. The tax treatment will depend on the nature of the returns (that is, whether the returns have characteristics similar to dividends, interest or income), and the purpose of the holder in acquiring the tokens.

GST treatment of digital tokens

The GST treatment of sales and purchases of tokens as part of an ICO primarily depends on whether

it meets the definition of digital currency, security or something else. Generally speaking, if the token is:

• a digital currency, it is treated the same way as money, and no GST will apply to sales of the token;

• security (for example, it is a share, derivative or managed investment scheme), no GST will apply to sales of the token; or

• neither a digital currency nor security, GST may apply to sales of the token. Other circumstances, including whether the parties are, or are required to be, registered for GST, will determine the GST treatment.

CONSULTATION QUESTIONS

ATTACHMENT A: TAX TREATMENT OF DIGITAL TOKENS

Income tax treatment for investors

This section considers the tax treatment applying to cryptocurrency (or tokens) that may be issued as part of an ICO to individual investors.

This tax treatment is not specific to ICOs, but applies generally to the acquisition and disposal of cryptocurrency, and may differ depending on the cryptocurrency’s characteristics and use. There may also be tax consequences that arise in relation to returns or flows of value that may be received by taxpayers who hold tokens that have been acquired through an ICO. The tax treatment in these circumstances will depend on the nature of the returns (for example, whether they have characteristics similar to dividends, interest or income), and the purpose of the holder in acquiring the tokens.

Cryptocurrency acquired as an investment

In general, cryptocurrency (including when acquired through an ICO as a coin or token) is considered an asset for tax purposes, and any capital gains arising may be subject to capital gains tax (CGT) at marginal tax rates on disposal. Cryptocurrency is considered to be disposed of when it is sold, traded or exchanged. For example, this can include converting cryptocurrency to a fiat currency such as Australian dollars, using it to obtain goods and services or exchanging one cryptocurrency for another cryptocurrency.

If a capital gain is made on disposal, the 50 per cent CGT discount may apply to capital gains on cryptocurrency held for a period of 12 months or longer. The CGT discount means that any capital gains made on the disposal of cryptocurrency (after offsetting any capital losses, including any net capital losses from previous years) are reduced by 50 per cent, so that tax is only paid by the individual at marginal rates on the balance.

Cryptocurrency acquired through a chain split

Cryptocurrencies may undergo what is often known as a ‘fork’, or what we refer to in this appendix as a chain split. A chain split occurs when the blockchain for a cryptocurrency diverges into two paths, resulting in the creation of new crypto currency and associated blockchain. The creation of Bitcoin Cash from Bitcoin is an example of a chain split.

A chain split may result in holders of cryptocurrency receiving a new cryptocurrency. This new cryptocurrency is in addition to their existing holdings of cryptocurrency and is a direct result of the

chain split. If individuals hold cryptocurrency as an investment and receive a new cryptocurrency as a result of a chain split, they will not derive ordinary income or make a capital gain at the time they receive the new cryptocurrency. However, they will make a capital gain when they dispose of the new cryptocurrency. For the purposes of working out the capital gain, the cost base of the new cryptocurrency received is zero.

If the new cryptocurrency is held as an investment for 12 months or more, individuals may be entitled to receive the 50 per cent CGT discount.

Cryptocurrency held as a personal use asset

Cryptocurrency that is acquired and used solely for the purchase of goods and services for personal use or consumption may be considered a personal use asset. Capitals gains on personal use assets acquired for less than $10,000 are disregarded for tax purposes. However, all capital losses made on

personal use assets are disregarded.

Income tax treatment for issuers

This section considers the current tax treatment applying to cryptocurrency (or tokens) that may be issued as part of an ICO from the issuer’s perspective. The tax treatment would ordinarily follow the attributes of the offering. For example, ICOs could be undertaken in the form of a managed investment scheme, in the form of an offer of shares, offer of a derivative, or non-cash payment facility (potentially for future services to be provided by the issuer).

Just like any other transaction or event, the existing tax rules will apply to ICO arrangements. The tax treatment of the ICO will depend on how the ICO is structured and operated, the characteristics of the token, products and/or services being offered and the rights and obligations between the parties. Factors potentially impacting the tax treatment can include whether there are voting rights, rights to share in profits, rights to receive certain products or services, or a right to repayment of the

investment. As such, there is not a single tax outcome that will apply to all ICOs.

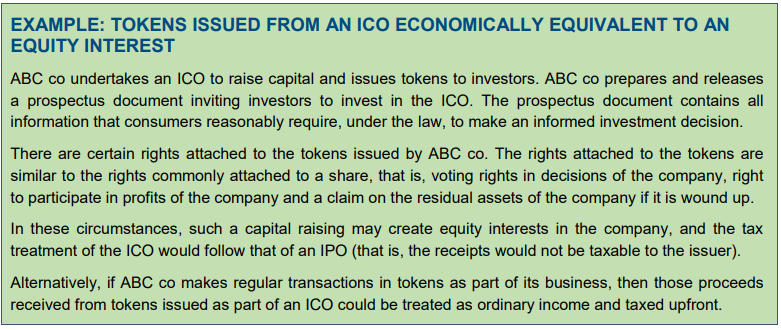

Tokens economically equivalent to debt or equity interests

The tax law contains tests to determine whether a particular interest is a debt interest or an equity interest (or neither) for tax purposes. These ‘debt and equity tests’ may impact on the tax treatment of the proceeds of the ICO (both in the hands of the issuer and the holder), including whether a return on an interest in an entity may be frankable and non-deductible to the issuer (like a dividend), or whether it may be deductible to the issuer and not frankable (like interest).

Broadly, in order for an interest to be classified as an equity interest, the interest must carry a return

that is contingent on the economic performance of the issuer. Conversely, if the interest carries an obligation that the issuer is required to return to the holder an amount at least equal to the amount invested, then the interest may be treated as a debt interest.

Treatment as capital or trading stock, and other considerations

In certain circumstances, the proceeds could form the principal of a debt or equity interest (and not taxed upon receipt), whereas in other circumstances tax will be payable upfront on the proceeds of the ICO if the proceeds are ordinary income.

If the issuer of the tokens makes regular transactions in tokens, it is possible that the proceeds could

be seen as forming part of some trading activity such that the ICO proceeds could be taxed as ordinary income.

Depending on the attributes of the arrangement, other tax consequences may arise for the issuer of

the tokens, for example:

• Where the tokens are issued in respect of prepayment for a service, the issue proceeds are likely to be assessable to the issuer.

• Proceeds from tokens that are issued as an offer of a derivative could be subject to tax under the taxation of financial arrangement rules and may form part of the cost base of the financial arrangement.

• Where the tokens are issued to employees of the issuer in relation to their employment, those tokens may constitute to be a benefit that could be subject to the fringe benefit tax provisions.

Given the variety in how these arrangements can be structured, there is no single manner in which ICO proceeds are taxed.

GST on sales of cryptocurrency

The GST treatment of sales and purchases of cryptocurrency as part of an ICO primarily depends on

whether it meets the definition of digital currency, security or something else. Whether parties are registered for GST, or are required to register for GST, will also affect the GST treatment. Generally speaking, if the cryptocurrency is:

• a digital currency, it is treated the same way as money, and no GST will apply to sales of the cryptocurrency;

• security (for example, it is a share, derivative or managed investment scheme), no GST will apply to sales of the cryptocurrency; or

• neither a digital currency nor security, GST may apply to sales of the cryptocurrency. Other circumstances, including whether the parties are, or are required to be, registered for GST, will determine the GST treatment.

We’re an authoritative group of subject experts and enthusiasts who are evangelizing the new skills research and development, use cases, products and knowledge for a better world.